PHOTOGRAPHY: GETTY IMAGES / ALAMY

On the international level, prepaid

debit cards allow travelers to load up

multiple currencies onto a single card,

offering a payment method in each

c o u n t r y t h e t r a v e l e r w i l l v i s i t .

Essentially, these prepaid travel cards

are the modern equivalent of traveler’s

c h e c k s b u t w i t h o n e i mp o r t a n t

difference — they can be canceled and

replaced immediately if lost.

Prepaid international travel cards

operate using the VISA or MasterCard

network, and you use them just as you

would use a regular credit card.

Typically they are protected by the chip-

and-PIN system but because they are

not directly linked to your bank account,

any losses through fraud or theft are

limited to the value stored on the card.

There is increasing evidence that

globetrotters are actively seeking out a

cashless ecosystem to simplify trips.

Thomas Cook India, for example,

Sweden is leading the race to become the

world’s first cashless country.

recently revealed a 25 percent growth in

its prepaid card services. While the

cards offer substantial gains in security

and flexibility, users should be aware

that exchange rates offered by providers

may not be as competitive as spot rates

offered by banks.

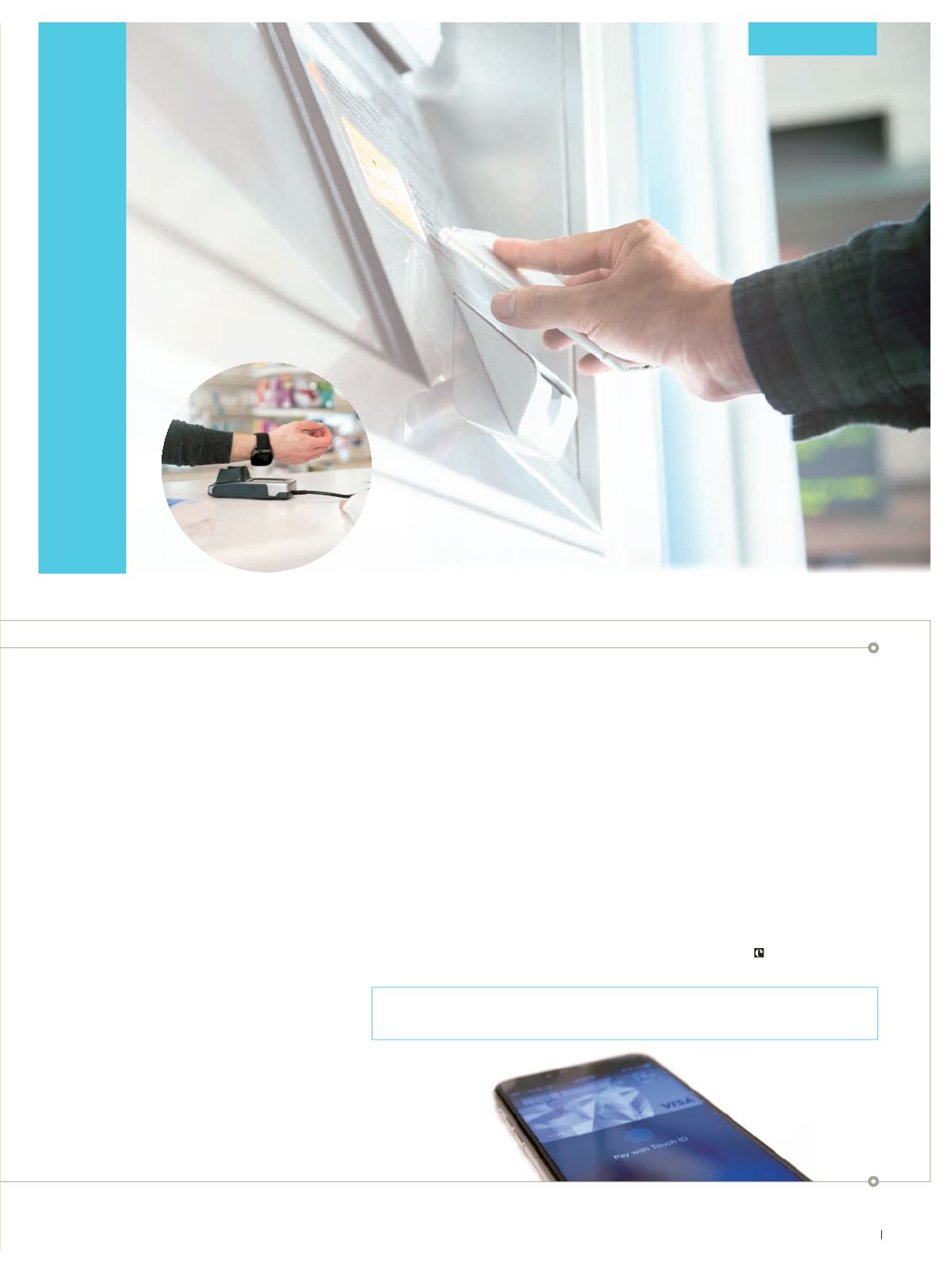

Travel-card use is certainly gaining

momentum, but the technology is set to

be e c l i p s ed by sma r t phone s and

smartwatches. Near-field communication

(NFC) is capable of emulating travel

cards, giving users the option of paying

for goods and services using Google

Wallet or ApplePay. And if that wasn’t

enough, financial technology is on the

verge of tearing down geographical

boundaries to create a global currency.

Blockchain-based payment systems such

as Bitcoin offer the tantalizing prospect

of being able to pay for anything in any

country at the push of a button. Still in its

infancy, Bitcoin may well be the

international currency of choice should

the world’s big financial institutions

decide to adopt it.

45

enVoyage